No Deal: Adobe and Figma Breakup 💔

Breaking down the Adobe-Figma breakup

And just like that… after 15 months of review, the highly anticipated merger of Adobe and Figma has been called off! Last Monday, both companies announced their mutual agreement to terminate the $20 billion merger. Why? Insurmountable regulatory and antitrust hurdles. Figma CEO, Dylan Field, explained that the two companies “no longer see a path toward regulatory approval”. Instead, Adobe will pay a whopping $1 billion termination fee. 💸

All eyes have been on BigTech recently, and the break up of Adobe-Figma may just be the tip of the iceberg. Are regulators finally gaining some teeth? In this article, I’ll unpack the details about why antitrust authorities clamped down on the proposed merger and share a few perspectives on what this means for tech companies in 2024 and beyond. Spoiler: Competition is in. AI is changing the rules. Europe is leading. And US antitrust law might need an overhaul.

A Vision for Collaborative Creativity *Pending Regulatory Approval 🚫

As a quick background, Figma is a buzzy design software startup founded in San Francisco in 2012. It’s most well known for 2 major products: Figma Design which offers software for teams to design products together and FigJam which is an online whiteboarding tool. Adobe is the acquisitive company behind Photoshop, Illustrator and several other creative design tools. Together, their vision was to join forces and usher in a new era of “collaborative creativity”. Or to take the regulator’s perspective: monopolize the design software market. Adobe wanted to offer Figma’s web-based collaboration tools to its large customer base and use Figma’s technology to build on its own products. Figma saw a much faster path to achieve their vision to “eliminate the gap between imagination and reality”. A lavish exit didn’t hurt either.

In deals, one oft-overlooked subtlety is the distinction between mergers and acquisitions. M&A is like PB&J. They are related, but distinct. When regulatory approval is expected to be long and complex, companies prefer mergers because the deal is locked in during the lengthy review process. Acquisitions, on the other hand, are better suited for simple review processes, because closing must wait for regulatory approval. This nuance is crucial in understanding the dynamics of the Adobe-Figma merger, where the extended review process and regulatory scrutiny played a much more significant role than initially anticipated.

On September 15, 2022, Adobe and Figma announced a definitive merger agreement, through which Adobe would buy Figma for roughly $10 billion in cash and $10 billion in stock. At the time, the $20 billion offer was 2x Figma’s valuation, which set off alarm bells across regulatory authorities in Europe and the US. The transaction was slated to close a year later - contingent upon receiving regulatory approvals from antitrust authorities. Traditionally, “pending regulatory approval” is viewed as a mere formality. While the process can be rigorous and time-consuming, it's not typically considered a substantial check on a proposed merger. But that might be changing… especially in Europe.

Competition Authorities: CMA Leads the Pack 👑

The Competition and Markets Authority (CMA) is the UK’s primary competition watchdog. In May 2023, they launched a merger inquiry to investigate whether the Adobe-Figma merger would stifle competition and reduce innovation under the merger provisions of the Enterprise Act of 2002. They assessed the deal relative to prevailing market conditions of competition which involves both Adobe and Figma continuing to evolve, adapt, and innovate. In parallel, the European Commission also reviewed the deal under the EU Merger Regulation after receiving requests from 16 member states and the United States Department of Justice also amped up its own scrutiny (though the DoJ had not filed an antitrust suit). Still, the UK’s CMA led the charge.

CMA’s Chief Concern: Less Competition 🎯

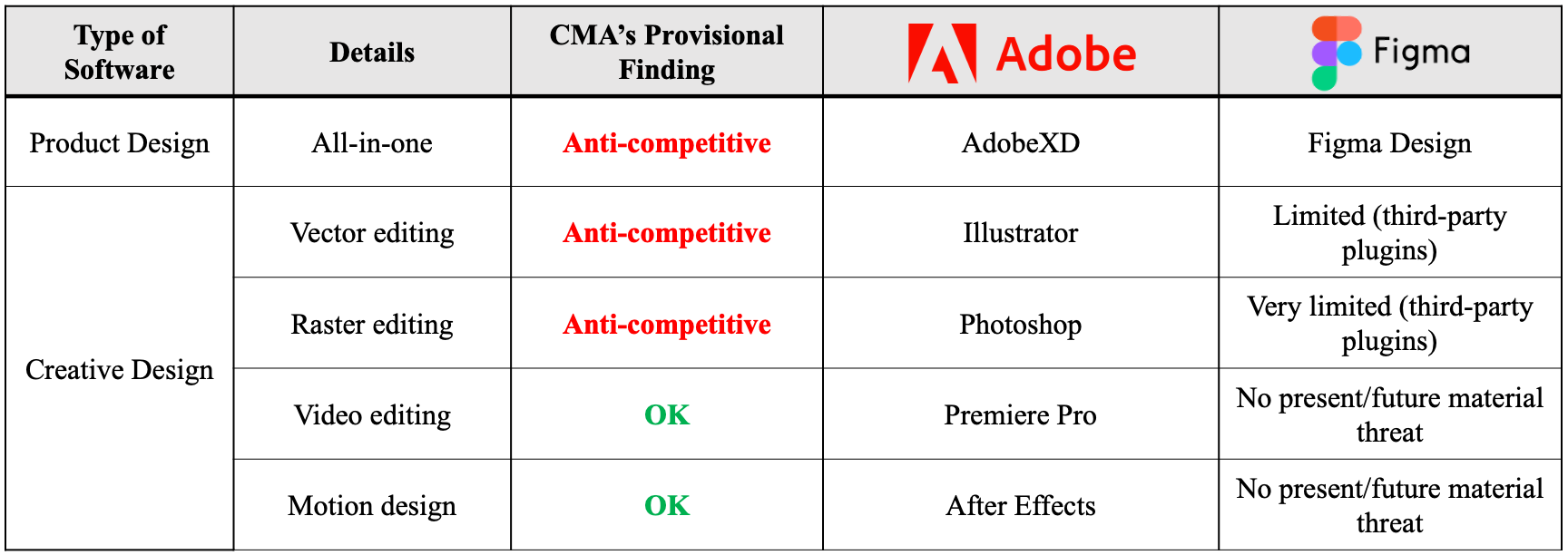

Specifically, the CMA went hunting for instances of substantial lessening of competition - “SLCs”. They were concerned about potential SLCs in the supply of (1) product design and (2) creative design software. Product design software is used to design websites, mobile applications and digital marketing material - basically anything that involves user interactions. The process typically involves sketching, wire-framing, mockups, prototyping, and eventually, a handoff to developers. These tools don’t create the applications directly, but give designers an idea for how the final product will look and work. Collaboration is critical to allow all creative professionals, developers and customers to work together to achieve a particular vision. On the other hand, creative design software is used to actually create assets such as photos, illustrations, web graphics, app icons or videos. Typically, this includes vector editing for creating content, raster editing for adjusting or retouching images, video editing for cutting and enhancing existing materials, and motion design for adding visual effects to video content.

(1) Product Design: Advantage Figma.

Though both Adobe and Figma have all-in-one product design software geared towards professional users, Figma is the clear market leader. Its web-based product, Figma Design, primarily competes with AdobeXD, which is Adobe’s desktop-based offering. In a 2023 survey asking 3,000+ designers what tools they used for UI design, Figma was the winner by a landslide. Adobe and Sketch were mostly viewed as backup tools.

In 2021, Figma also started offering a collaborative whiteboarding tool called FigJam to help teams brainstorm and ideate together. Adobe had no presence in whiteboarding.

Bottom line: designers love Figma. The tool solved a hard collaboration problem and offered a seamless UI in ways that incumbent companies failed to do. As a result, Adobe really wanted Figma. Adobe’s own product design software, AdobeXD, was placed in maintenance mode in 2022. They withdrew resources and stopped offering it as a standalone product (only as part of the Creative Cloud All Apps bundle). Adobe also cancelled an internal whiteboarding project called Project Spice which was focused on developing an infinite canvas for mixed-media asset ideation and creation. Some have speculated that both decisions (sunsetting AdobeXD and Project Spice) were taken in anticipation of a successful merger.

(2) Creative Design: Advantage Adobe.

Although Figma won designer’s hearts, Adobe set the industry standard in creative design. They offer standalone products and subscription-based bundles across several types of creative design software and reap the benefits of technological lock-in. Their flagship apps include: Illustrator for vector editing (creating content), Photoshop for raster editing (image enhancements), PremierePro for video editing, and After Effects for video enhancements and animated graphics. In vector and raster editing, Adobe enjoys a virtually unrivaled market position. In video editing and enhancement, Adobe still leads the market but faces strong competition from Apple and Blackmagic for video editing and Apple and Blender for motion design.

Conversely, Figma lacked its own standalone creative design software. Instead, they sprinkled in some modest creative design functionalities as part of Figma Design (e.g., drawing icons, spot illustrations, adjusting exposure, scaling/sizing, basic animations). Importantly, Figma had contemplated developing or acquiring this capability, which signaled potential direct competition with Adobe. For Adobe, the merger was a strategic marriage aimed at addressing a current threat in design software and an imminent threat in creative design.

The Combo: A Figma of Adobe’s Imagination 🍥

On November 28, the CMA provisionally found competition concerns related to Adobe acquiring Figma. They identified three potential SLCs: one in all-in-one product design and two in creative design (vector and raster editing).

After expressing concerns about network effects strengthening Adobe’s position in creative design and Figma’s in product design, the CMA suggested an alternative structural remedy: divest Figma Design and work to eliminate all SLCs. But recall, Figma Design was the prized strategic asset that Adobe coveted! No remedy package would be able to preserve the benefits of the deal AND ease regulatory concerns. The CMA’s proposal was nothing more than a hollow olive branch. It was the equivalent of asking Adobe to part ways with their crown jewel. Predictably, Adobe refused to make these accommodations and both parties agreed to terminate the deal.

The termination of Adobe-Figma due to regulatory challenges raises several questions about the trajectory of BigTech M&A and startups in the future. The question on everyone’s mind is what next? A few thoughts: (1) competition is making a comeback (2) AI is changing the rules (3) Europe continues to lead and (4) US antitrust law might need an overhaul.

1️⃣ Competition Is In (and Figma Looks Good) 👀

Moving forward, Figma and Adobe will have to compete. But it’s not necessarily a level playing field. Despite a year of uncertainty with the pending merger, Figma had a prolific 2023. They continued to expand and launched several new features including variables, advanced prototyping, and developer mode. They’ve hired 500 new people (“figmates”) since September 2022, and also acquired an AI company called Diagram in June. In addition, the 1-billion-dollar termination fee is jet fuel for Figma. The fee is 3x the amount they raised in VC dollars over their 10+ year history. It’s the equivalent of a huge exit (without actually having to exit) and practically gives them a dilution free billion-dollar round of financing. Conversely, Adobe lost a critical opportunity to buy a rival whose web-based tools have emerged as a real threat. They also withdrew resources from AdobeXD and shelved ProjectSpice. Although some have suggested that Adobe may secretly be relieved since they acquired Figma at a peak market price, they still face an uphill battle to revamp their product design and collaboration tools to truly compete.

Regardless of the outcome between Adobe and Figma, this is a huge win for designers. For years, designers have lamented the high price of Adobe’s creative suite. But switching options have been limited because Adobe’s pricing, however high, has set the industry standard. An Adobe-Figma merger would probably have resulted in a more expensive software subscription that forced creators and designers to pay an even higher toll to access Adobe’s creative suite.

2️⃣ AI Is Changing the Rules: Coordination > Creation 🤝

In the age of generative AI, designer/creator priorities have shifted. Value lies not in creating content, but in effective coordination across the various aspects of content-related work. The AI craze has ushered in new products/tools from both Adobe and Figma. Adobe’s new product, Firefly, has been all the rage. It enables AI-assisted creative expression and is embedded within Adobe’s Creative Cloud offering. Figma added some AI functionality to FigJam to speed up design diagramming, brainstorming, and summarizing. But it barely holds a candle to Adobe Firefly. As AI shifts the value canvas towards enabling better collaboration over creation, the players that can bake AI seamlessly into creative workflows are well-positioned to win.

3️⃣ Europe Regulates, While America Innovates ⚖️

The UK/EU has emerged as a clear BigTech regulatory leader this year. Figma-Adobe is one among a series of BigTech transactions that have received regulatory scrutiny from the CMA. They also reversed Meta’s $400 million acquisition of Giphy and heavily investigated Microsoft’s $69 billion purchase of “Call of Duty” maker Activision-Blizzard.

Comparatively, America continues to be late to the party (and aloof upon arrival). The US antitrust authorities, the FTC and DOJ, used the UK to do it’s dirty work with Adobe and Figma. In a statement last week, Assistant Attorney General Kanter basically gave the PR equivalent of a pat on the back to the CMA regarding its Adobe-Figma findings. But this is not new. US authorities have consistently championed the dogma of innovation and permitted massive consolidation. They have been reliably (and some would say, intentionally) slower and less forceful than European counterparts. With the rise of Lina Khan and the Neo-Brandesian movement, perhaps the US will start to mirror a more interventionist stance.

4️⃣ We Need a “Bits, Not Atoms” Approach to Antitrust 🖥️

To sum up the current state of antitrust affairs: Adobe can’t buy Figma. But Microsoft is allowed to buy Github and Activision-Blizzard. And Facebook is allowed to buy WhatsApp and Instagram. Something isn’t quite adding up…

Modern antitrust law is built on an “atoms, not bits” approach to consumer welfare. It’s well designed to tackle questions like: are firms driving prices up through cartel behavior? But doesn’t apply as easily when companies are creating free products for digital users. The prevalence of freemium business models, low or zero switching costs, and growing concerns over data privacy all suggest that it is time to reevaluate antitrust in the digital world and explicitly consider the issues raised by tech company business models.

Although stricter regulatory scrutiny would challenge the startup playbook of building strategic assets and hoping for an acquisition, perhaps a system that moves closer to “IPO or bust” isn’t all bad news. Instead, it may prompt a timely reevaluation of the unquestioned pursuit of innovation and encourage more groundbreaking Figma-style innovation and genuine business building.

P.S. For some more creative analysis, check out this “Business Wire” article: